According to the Small Business Administration, “borrowers may be eligible for loan forgiveness” as long as “the funds were used for eligible payroll costs, payments on business mortgage interest payments, rent, or utilities during either the 8- or 24-week period after disbursement.” Yet, with the immense ambiguity surrounding forgiveness legislation, along with constant release of new information and different forms, it can be overwhelming to understand how to start the application process.

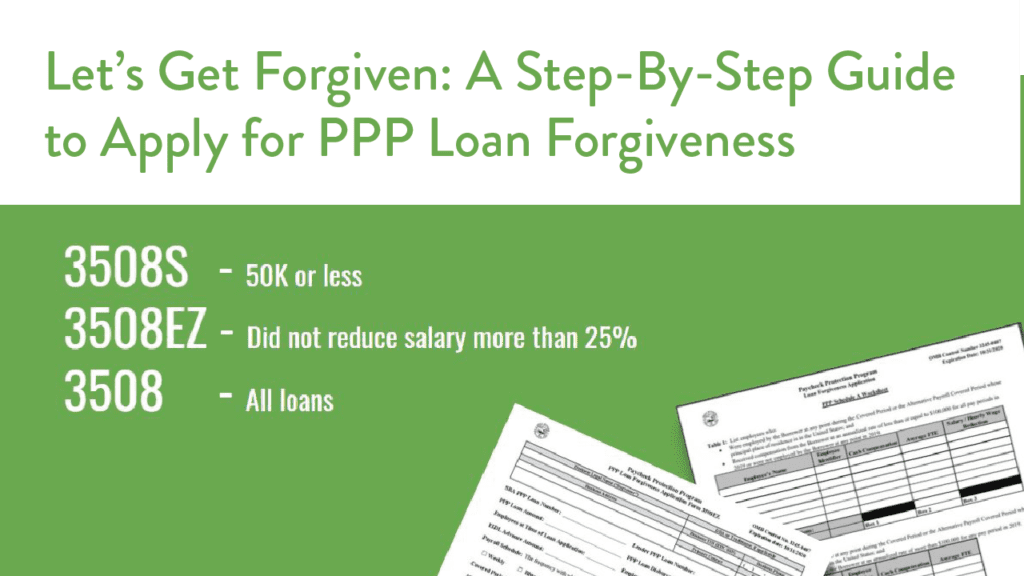

Let’s make things a little easier. Under current legislation, there are three main form options to consider: Form 3508, 3508EZ and 3508S. Don’t know which one to choose? Below is a breakdown of each form.

3508S Form

If your loan is under $50,000, then the 3508S Form is the one for you. Those that use Form 3508S are exempt from reductions in loan forgiveness amounts based on reductions in their full-time equivalent (FTE) employees and their wages.

The 3508S Form is the most simplified forgiveness application, as it requires fewer calculations and documentation. However, don’t fall for the common mistake of not submitting your payroll records – your Covered Period and Alternative Period must still be established.

3508EZ Form

The other simplified forgiveness application is Form 3508EZ. The EZ Form is designed for businesses that meet at least one of the following criteria:

1. Business owners are self-employed and have no employees.

2. Businesses did not reduce the salaries or wages of their employees by more than 25% and did not reduce the number of hours their employees worked.

3. Businesses did not reduce salaries or wages of their employees by more than 25% and were unable to operate due to COVID19 restrictions.

To learn how to fill out both the 3508S and the 3508EZ Form, follow along with Drew Schildwachter, COO at ConnectPay, as he walks you through each section of the application.

3508 Form

The original, and most complex, forgiveness form is required if you do not qualify for the other simplified forms. Only a small minority of small businesses will need to use the standard 3508 form.

With more calculations required than any other application, this is this most detailed and personalized form. Please reach out individually if you need assistance or have additional questions.

And Don’t Forget About the Safe Harbors!

Once you’ve picked out the right form to use, keep in mind that the PPP Flexibility Act established additional safe harbors to help more small businesses achieve forgiveness, even if they did not meet the original established criteria. With these safe harbors in place, some businesses may still have their loans forgiven, despite reducing their employee headcounts or wages during COVID.

Safe Harbor 1: Businesses that weren’t able to operate at the same level between February 15, 2020 and the end of the Covered Period due to compliance guidelines issued by the federal government, as well as state and local government orders, would qualify for a safe harbor.

Safe Harbor 2: If the borrower reduced its full-time equivalent (FTE) employee levels in the period beginning in February 15, 2020 and ending in April 26, 2020 and then the borrower restored its FTE employee levels by no later than December 31, 2020, the borrower would qualify for a safe harbor.

There are also 6 FTE reduction exceptions, which do not reduce the borrower’s forgiveness amount. These exceptions include:

1. The borrower made a good faith written offer to rehire an employee, but the offer was rejected by the employee.

2. An employee was fired for cause.

3. An employee voluntarily resigned.

4. An employee voluntarily requested and received a reduction in their hours.

5. The borrower made a good faith written offer to restore any reduction in hours at the same salary or wages, but the offer was rejected by the employee.

6. The borrower was unable to hire similarly qualified employees for unfilled positions by December 31, 2020.

If you’re looking for further guidance on PPP Loan Forgiveness, make sure to check out the full version of our webinar PPP Loan Forgiveness: Where Are We Now? If you also need help navigating the Employee Retention Credit, you can visit our ERC FAQ page!